The federal government recently announced two new mortgage rules coming to Canada to improve housing affordability. These two New Mortgage Rules are coming on December 15, 2024.

Change #1 – Increasing the $1 million price cap for an insured mortgage to $1.5 million

This rule has been introduced to reflect the current housing realities and help more Canadians enter the market. This means that down payments for homes within that budget will decrease. Insured mortgages require a 20% down payment minimum, but the structure is changing now.

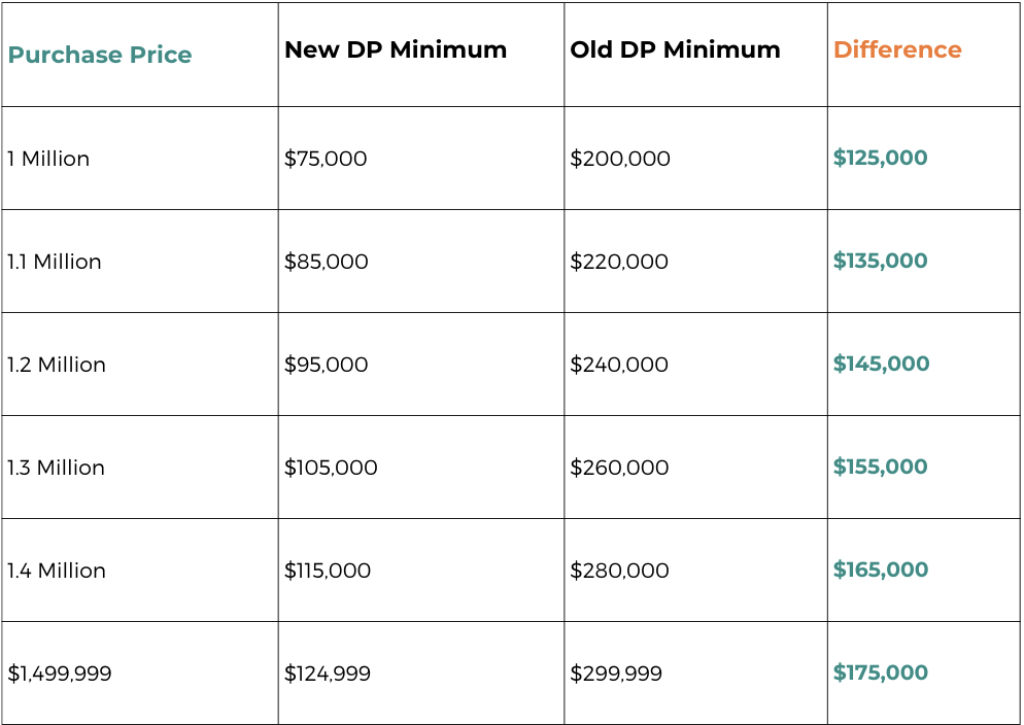

Previous Down Payment Structure

- 5% for the portion of the purchase price up to $500,000, and

- 10% for the portion between $500,000 and $999,999

- 20% total for anything 1M and up

New Down Payment Structure

- 5% for the portion of the purchase price up to $500,000, and

- 10% for the portion between $500,000 and $1.5 million

Summary of New vs Old Mortgage Changes

20% of homes in Canada are estimated to be worth between $1,000,000 and $1,499,999. This change is particularly significant for buyers in major urban markets like Toronto and Vancouver, where home prices often exceed the previous $1-million cap. In my marketplace of the Fraser Valley, we have a lot of homes priced between this bracket. Most are entry-level detached homes and larger townhomes.

This policy change is for everyone, not just first-time home buyers. The down payment structure changes above are substantial. This change makes the barrier to entry much easier, reducing the amount needed. However, keep in mind that purchasers will still have to qualify. This means even if you have the down payment amount, lenders will still take into account your income, credit score and debt service ratios. So, I think it will be a challenge for people to qualify given the new down payment guidelines because of how we qualify purchasers here in Canada.

A good rule of thumb when wondering what you might be pre-approved for is to multiply your income by 4.

I do not think this will have a drastic change on the real estate market because most people who are purchasing within that bracket have previously owned a home and are moving up. Generally, first-time home buyers are looking for under 1M..unless, of course, they have help from family.

What this will do is get the market moving for homes 1-1.5 which in my marketplace are a lot of them (and that s the case with most metropolitan areas).

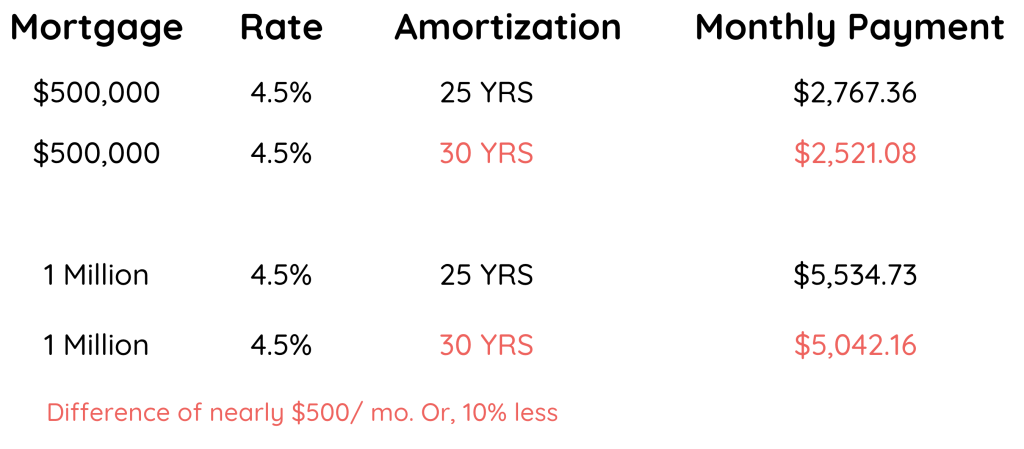

Change #2 – Extending the amortization from 25 years to 30 years

Amortization is the time it takes someone to pay off their mortgage. Expanding an amortization period stretches out the time someone has to pay off their mortgage, reducing the cost of monthly mortgage payments. Expanding amortization also means the purchaser will be paying more interest over time.

Effective December 15th, the federal government is expanding eligibility for 30-year mortgage amortizations to all first-time homebuyers (regardless of their downpayment), and to all buyers of new builds (pre-sales).

Old Rules

For anyone putting down less than 20%, max amortization was 25 years unless purchasing pre-sale, then it was 30 years. If a purchaser puts more than 20% down, only then can they get a 30-year amortization.

New Rules

First-time home buyers can get a mortgage with a 30-year amortization regardless of their downpayment. So, even if they put less than 20% (insured mortgage) down for a resale and/or pre-sale, they are still eligible for a 30-year amortization.

Anyone (not just first-time home buyers) purchasing new construction is also eligible for a 30-year amortization, even if they are putting less than 20% down.

Payment Break Down of The Extra 5-Year Mortgage Amortization

This new amortization rule allows first-time home buyers to qualify for roughly 10% more than they would have otherwise with a 25-year amortization. When you run the numbers is equivalent to 0.9% rate cut. You can look at the new amortization rules as a way to offset nearly half of the stress test – which makes you qualify at 2% higher than the posted rate.

Closing thoughts

The amortization extension should have more of an effect than the decreased downpayment structure up to 1.5M as most people who were buying in the 1-1.5M range are not first-time home buyers, therefore are usually putting 20% (insured mortgage) down or more because of the built-up equity in their previous home.

With the lower down payment amounts, be careful not to over-leverage yourself and take on too much debt.

It is interesting to see that when purchasing a new build, the 30-year amortization is allowed for everyone, regardless of your downpayment. This is a good thing as it will expand the buyer pool for new builds and encourage developers to continue building and providing housing which we desperately need to curb the housing shortage.